![]()

![]()

The goal of ycevo is to provide means for the

non-parametric estimation of the discount rate, and yield curve, of CRSP

Bond Data.

If you use any data or code from the ycevo package CRAN

release in a publication, please use the following citation:

Bonsoo Koo, Nathaniel Tomasetti, Kai-Yang Goh and Yangzhuoran Fin Yang (2022). ycevo: Non-Parametric Estimation of the Yield Curve Evolution. R package version 0.1.0. https://github.com/bonsook/ycevo.

The package provides code used in Koo, La Vecchia, & Linton (2021). Please use the following citation if you use any result from the paper.

Koo, B., La Vecchia, D., & Linton, O. (2021). Estimation of a nonparametric model for bond prices from cross-section and time series information. Journal of Econometrics, 220(2), 562-588.

The package is in active development and will experience substantial changes.

The main functionality has been improved and adjusted in the past years. When we first prepared it for CRAN submission, we set the version to be 1.0.0. Several years later when we finally have done it, we dialled it back to 0.1.0 in our realisation that the API is far from stable. It was not a good practice but it is better to do this sooner when it is not well publicised than to wait until more damages are made.

Note this first public release is not backward compatible with any fork before 2022 with version 1.0.0. These forks should be “updated” to 0.1.0 for a correct implementation.

You can install the released version of ycevo from CRAN with:

install.packages("ycevo")You can install the development version from GitHub with:

# install.packages("devtools")

devtools::install_github("bonsook/ycevo")library(ycevo)

library(tidyverse)

#> ── Attaching packages ─────────────────────────────────────── tidyverse 1.3.1 ──

#> ✓ ggplot2 3.3.6 ✓ purrr 0.3.4

#> ✓ tibble 3.1.7 ✓ dplyr 1.0.9

#> ✓ tidyr 1.2.0 ✓ stringr 1.4.0

#> ✓ readr 2.1.2 ✓ forcats 0.5.1

#> ── Conflicts ────────────────────────────────────────── tidyverse_conflicts() ──

#> x dplyr::filter() masks stats::filter()

#> x dplyr::lag() masks stats::lag()

library(lubridate)

#>

#> Attaching package: 'lubridate'

#> The following objects are masked from 'package:base':

#>

#> date, intersect, setdiff, union

# Simulate 4 bonds issued at 2020-01-01

# with maturity 180, 360, 540, 720 days

# Apart from the first one,

# each has coupon 2,

# of which half is paid every 180 days.

# The yield curve is sumulated fron `get_yield_at_vec`

# Quotation date is also at 2020-01-01

exp_data <- tibble(

qdate = ymd("2020-01-01"),

crspid = rep(1:4, 1:4),

pdint = c(100, 1, 101, 1, 1, 101, 1, 1, 1, 101),

tupq = unlist(sapply(1:4, seq_len)) * 180,

accint = 0

) %>%

mutate(discount = exp(-tupq/365 * get_yield_at_vec(0, tupq/365))) %>%

group_by(crspid) %>%

mutate(mid.price = sum(pdint * discount)) %>%

ungroup()

# Only one quotation so time grid is set to 1

xgrid <- 1

# Discount function is evaluated at time to maturity of each payment in the data

tau <- unique(exp_data$tupq/365)

# Estimated yield and discount

yield <- ycevo(

exp_data,

xgrid = xgrid,

tau = tau

)

yield

#> discount xgrid tau yield

#> 1 0.9801882 1 0.4931507 0.04057724

#> 2 0.9654370 1 0.9863014 0.03566294

#> 3 0.9515561 1 1.4794521 0.03356421

#> 4 0.9365043 1 1.9726027 0.03325614

# True yield

get_yield_at_vec(0, tau)

#> [1] 0.04057724 0.03566294 0.03356421 0.03325614

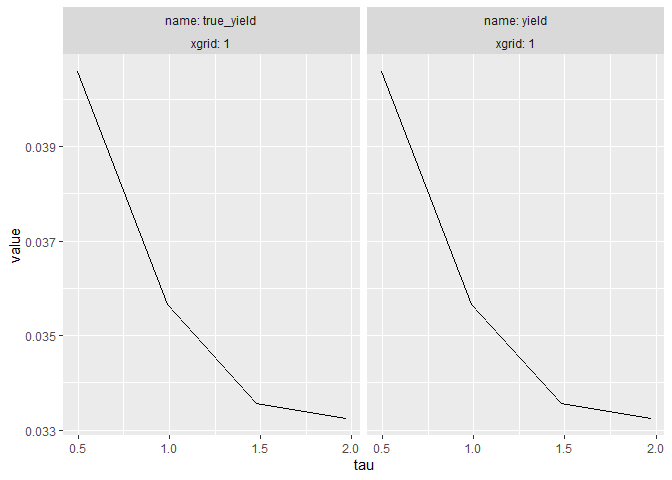

# Plot of yield curve

yield %>%

mutate(true_yield = get_yield_at_vec(0, tau)) %>%

pivot_longer(c(yield, true_yield)) %>%

mutate(xgrid = round(xgrid, 2)) %>%

ggplot() +

geom_line(aes(x = tau, y = value)) +

facet_wrap(name~xgrid, labeller = label_both)

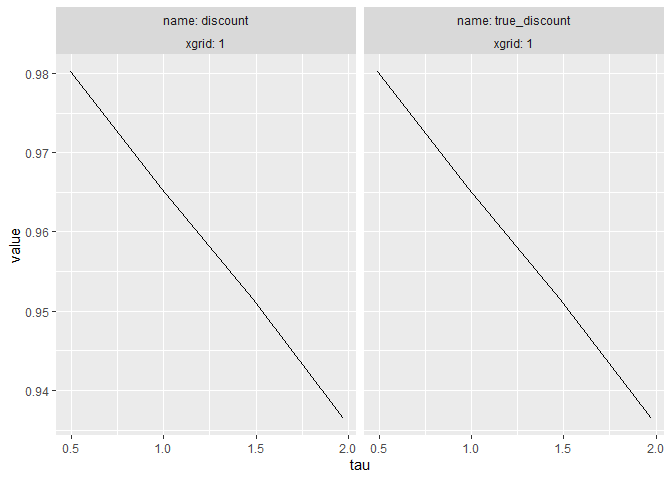

# Plot of discount function

yield %>%

mutate(true_discount = exp(-tau * get_yield_at_vec(0, tau))) %>%

pivot_longer(c(discount, true_discount)) %>%

mutate(xgrid = round(xgrid, 2)) %>%

ggplot() +

geom_line(aes(x = tau, y = value)) +

facet_wrap(name~xgrid, labeller = label_both)

This package is free and open source software, licensed under GPL-3